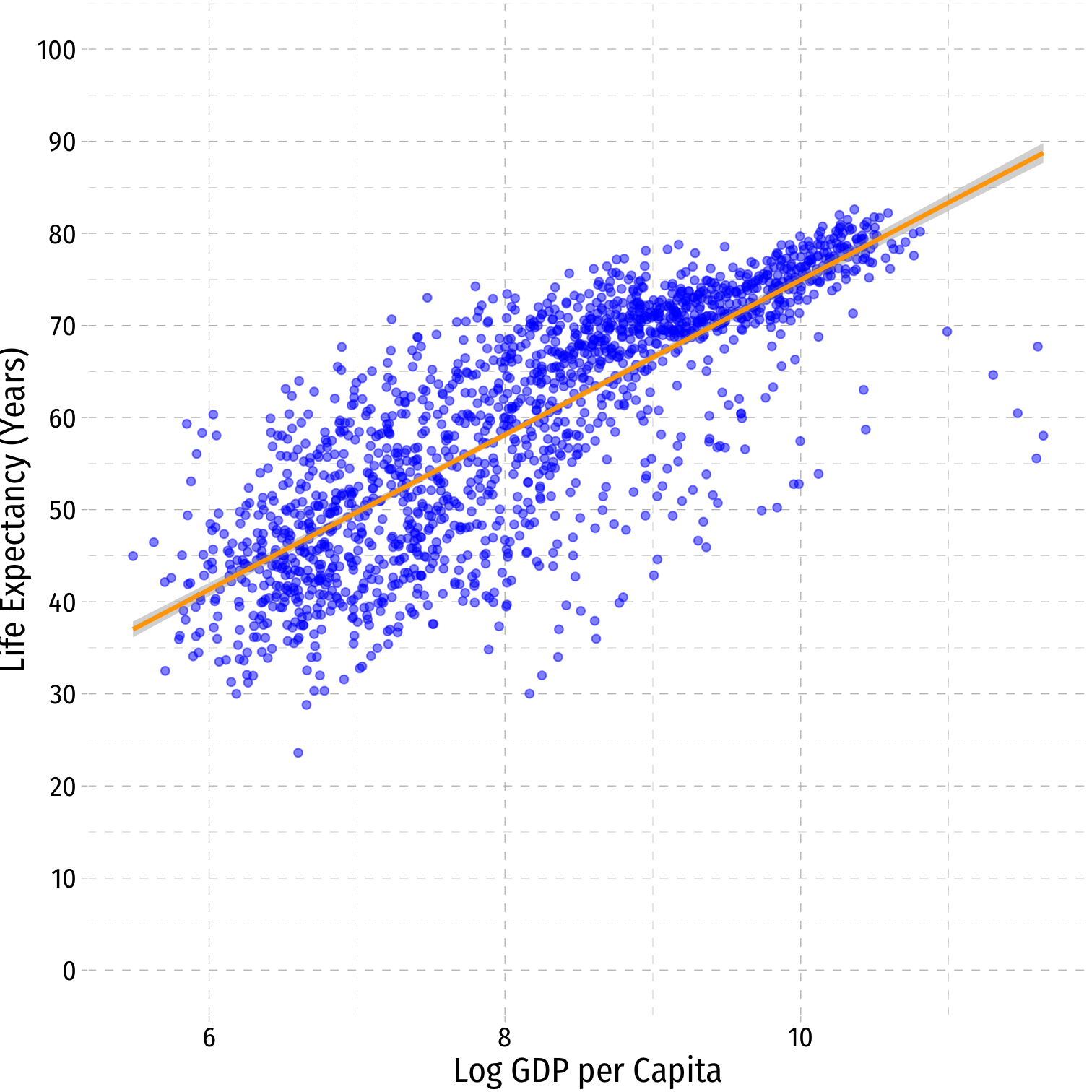

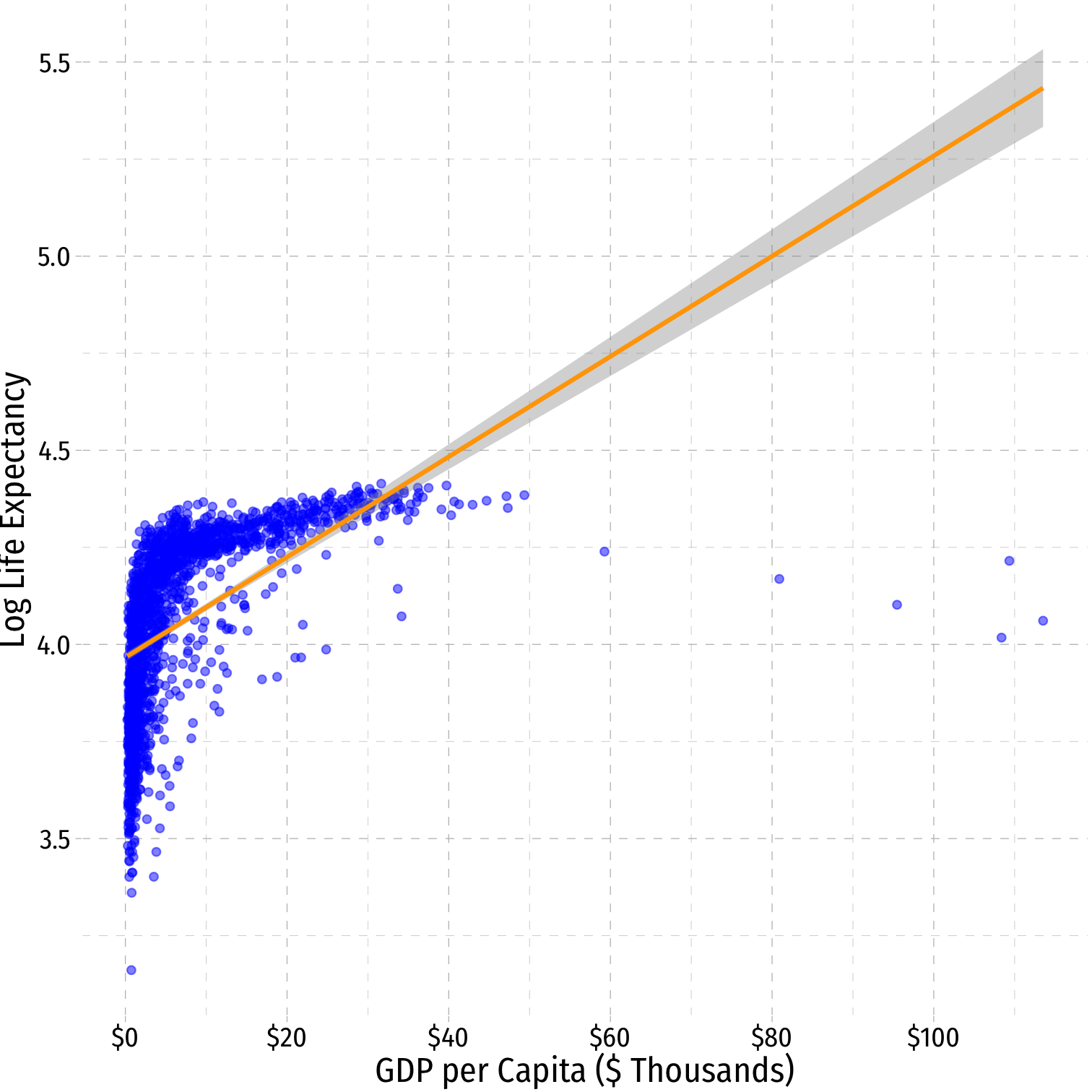

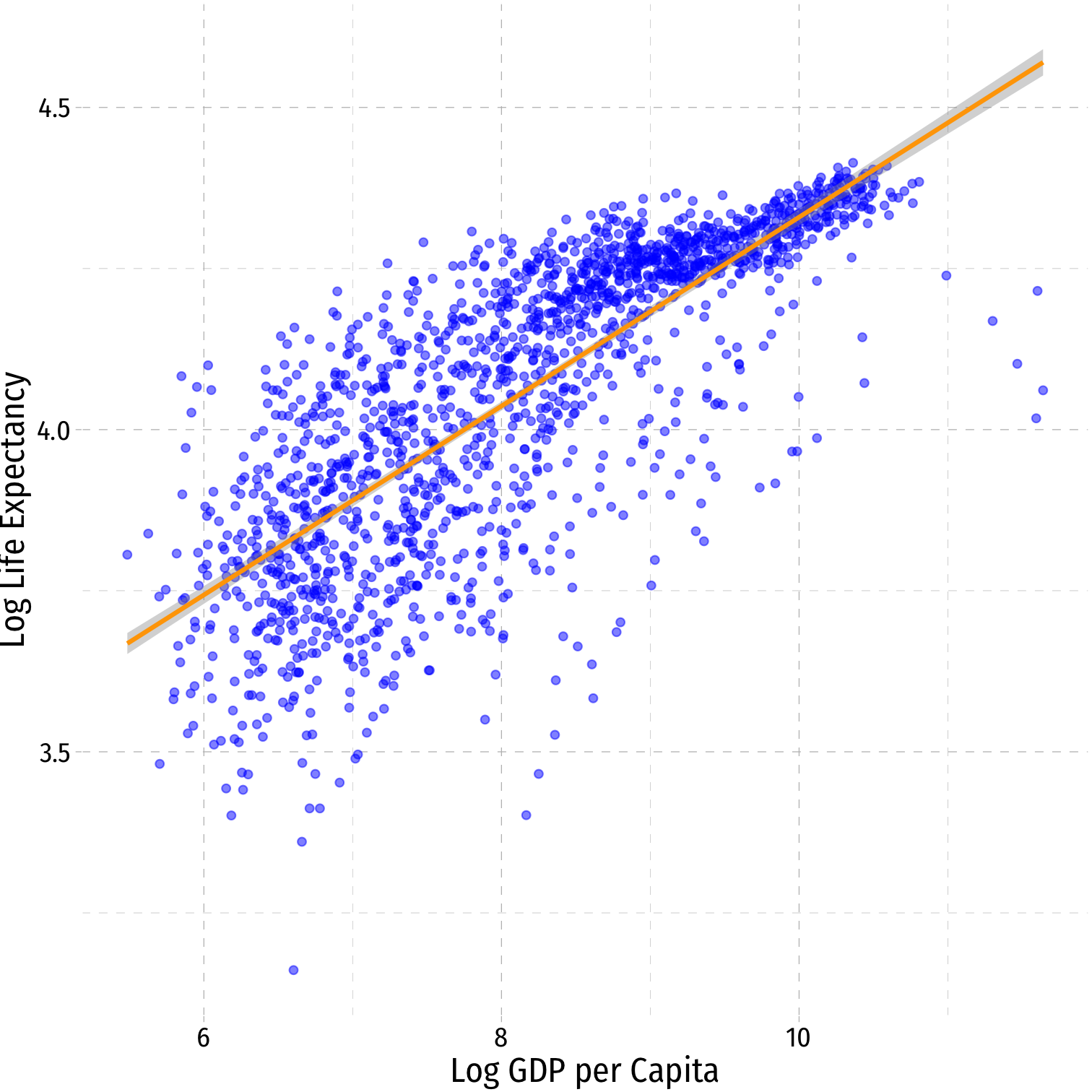

class: center, middle, inverse, title-slide # 3.9 — Logarithmic Regression ## ECON 480 • Econometrics • Fall 2020 ### Ryan Safner<br> Assistant Professor of Economics <br> <a href="mailto:safner@hood.edu"><i class="fa fa-paper-plane fa-fw"></i>safner@hood.edu</a> <br> <a href="https://github.com/ryansafner/metricsF20"><i class="fa fa-github fa-fw"></i>ryansafner/metricsF20</a><br> <a href="https://metricsF20.classes.ryansafner.com"> <i class="fa fa-globe fa-fw"></i>metricsF20.classes.ryansafner.com</a><br> --- class: inverse # Outline ### [Natural Logarithms](#7) ### [Linear-Log Model](#37) ### [Log-Linear Model](#47) ### [Log-Log Model](#58) ### [Comparing Across Units](#72) ### [Joint Hypothesis Testing](#78) --- # Nonlinearities .pull-left[ - Consider the `gapminder` example ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-1-1.png" width="504" /> ] --- # Nonlinearities .pull-left[ - Consider the `gapminder` example .quitesmall[ `$$\color{red}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP per capita}_i}$$` ] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-2-1.png" width="504" /> ] --- # Nonlinearities .pull-left[ - Consider the `gapminder` example .quitesmall[ `$$\color{red}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP per capita}_i}$$` `$$\color{green}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP per capita}_i+\hat{\beta_2}\text{GDP per capita}_i^2}$$` ] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-3-1.png" width="504" /> ] --- # Nonlinearities .pull-left[ - Consider the `gapminder` example .quitesmall[ `$$\color{red}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP per capita}_i}$$` `$$\color{green}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\text{GDP per capita}_i+\hat{\beta_2}\text{GDP per capita}_i^2}$$` `$$\color{orange}{\widehat{\text{Life Expectancy}_i}=\hat{\beta_0}+\hat{\beta_1}\ln \text{GDP per capita}_i}$$` ] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-4-1.png" width="504" /> ] --- class: inverse, center, middle # Natural Logarithms --- # Logarithmic Models .pull-left[ .smallest[ - Another useful model for nonlinear data is the .hi[logarithmic model]<sup>.magenta[†]</sup> - We transform either `\(X\)`, `\(Y\)`, or *both* by taking the .hi-purple[(natural) logarithm] - Logarithmic model has two additional advantages 1. We can easily interpret coefficients as **percentage changes** or **elasticities** 2. Useful economic shape: diminishing returns (production functions, utility functions, etc) ] .tiny[<sup>.magenta[†]</sup> Don’t confuse this with a .hi[logistic (logit) model] for *dependent* dummy variables.] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-5-1.png" width="504" /> ] --- # The Natural Logarithm .pull-left[ <img src="3.9-slides_files/figure-html/unnamed-chunk-6-1.png" width="504" /> ] .pull-right[ - The .red[exponential function], `\(Y=e^X\)` or `\(Y=exp(X)\)`, where base `\(e=2.71828...\)` - .blue[Natural logarithm] is the inverse, `\(Y=ln(X)\)` ] --- # The Natural Logarithm: Review I .smallest[ - **Exponents** are defined as `$$\color{#6A5ACD}{b}^{\color{#e64173}{n}}=\underbrace{\color{#6A5ACD}{b} \times \color{#6A5ACD}{b} \times \cdots \times \color{#6A5ACD}{b}}_{\color{#e64173}{n} \text{ times}}$$` - where base `\(\color{#6A5ACD}{b}\)` is multiplied by itself `\(\color{#e64173}{n}\)` times ] -- .smallest[ - .green[**Example**]: `\(\color{#6A5ACD}{2}^{\color{#e64173}{3}}=\underbrace{\color{#6A5ACD}{2} \times \color{#6A5ACD}{2} \times \color{#6A5ACD}{2}}_{\color{#e64173}{n=3}}=\color{#314f4f}{8}\)` ] -- .smallest[ - **Logarithms** are the inverse, defined as the exponents in the expressions above `$$\text{If } \color{#6A5ACD}{b}^{\color{#e64173}{n}}=\color{#314f4f}{y}\text{, then }log_{\color{#6A5ACD}{b}}(\color{#314f4f}{y})=\color{#e64173}{n}$$` - `\(\color{#e64173}{n}\)` is the number you must raise `\(\color{#6A5ACD}{b}\)` to in order to get `\(\color{#314f4f}{y}\)` ] -- .smallest[ - .green[**Example**]: `\(log_{\color{#6A5ACD}{2}}(\color{#314f4f}{8})=\color{#e64173}{3}\)` ] --- # The Natural Logarithm: Review II - Logarithms can have any base, but common to use the **natural logarithm `\((ln)\)`** with base `\(\mathbf{e=2.71828...}\)` `$$\text{If } e^n=y\text{, then } \ln(y)=n$$` --- # The Natural Logarithm: Properties - Natural logs have a lot of useful properties: 1. `\(ln(\frac{1}{x})=-ln(x)\)` 2. `\(ln(ab)=ln(a)+ln(b)\)` 3. `\(ln(\frac{x}{a})=ln(x)-ln(a)\)` 4. `\(ln(x^a)=a \, ln(x)\)` 5. `\(\frac{d \, ln \, x}{d \, x} = \frac{1}{x}\)` --- # The Natural Logarithm: Example .smallest[ - Most useful property: for small change in `\(x\)`, `\(\Delta x\)`: `$$\underbrace{ln(x+\Delta x) - ln(x)}_{\text{Difference in logs}} \approx \underbrace{\frac{\Delta x}{x}}_{\text{Relative change}}$$` ] -- .smallest[ .content-box-green[ .green[**Example**]: Let `\(x=100\)` and `\(\Delta x =1\)`, relative change is: `$$\frac{\Delta x}{x} = \frac{(101-100)}{100} = 0.01 \text{ or }1\%$$` - The logged difference: `$$ln(101)-ln(100) = 0.00995 \approx 1\%$$` ] ] -- .smallest[ - This allows us to very easily interpret coefficients as **percent changes** or .hi-purple[elasticities] ] --- # Elasticity .smallest[ - An .hi[elasticity] between any two variables, `\(\epsilon_{Y,X}\)` describes the .hi-purple[responsiveness] (in %) of one variable `\((Y)\)` to a change in another `\((X)\)` ] -- `$$\epsilon_{Y,X}=\frac{\% \Delta Y}{\% \Delta X} =\cfrac{\left(\frac{\Delta Y}{Y}\right)}{\left( \frac{\Delta X}{X}\right)}$$` -- .smallest[ - Numerator is relative change in `\(Y\)`, Denominator is relative change in `\(X\)` ] -- .smallest[ - .hi-purple[Interpretation]: a 1% change in `\(X\)` will cause a `\(\epsilon_{Y,X}\)`% chang in `\(Y\)` ] --- # Math FYI: Cobb Douglas Functions and Logs - One of the (many) reasons why economists love Cobb-Douglas functions: `$$Y=AL^{\alpha}K^{\beta}$$` -- - Taking logs, relationship becomes linear: -- `$$ln(Y)=\ln(A)+\alpha \ln(L)+ \beta \ln(K)$$` -- - With data on `\((Y, L, K)\)` and linear regression, can estimate `\(\alpha\)` and `\(\beta\)` - `\(\alpha\)`: elasticity of `\(Y\)` with respect to `\(L\)` - A 1% change in `\(L\)` will lead to an `\(\alpha\)`% change in `\(Y\)` - `\(\beta\)`: elasticity of `\(Y\)` with respect to `\(K\)` - A 1% change in `\(K\)` will lead to a `\(\beta\)`% change in `\(Y\)` --- # Math FYI: Cobb Douglas Functions and Logs .content-box-green[ .hi-green[Example]: Cobb-Douglas production function: `$$Y=2L^{0.75}K^{0.25}$$` ] -- - Taking logs: `$$\ln Y=\ln 2+0.75 \ln L + 0.25 \ln K$$` -- - A 1% change in `\(L\)` will yield a 0.75% change in output `\(Y\)` - A 1% change in `\(K\)` will yield a 0.25% change in output `\(Y\)` --- # Logarithms in R I - The `log()` function can easily take the logarithm .smallest[ ```r gapminder <- gapminder %>% mutate(loggdp = log(gdpPercap)) # log GDP per capita gapminder %>% head() # look at it ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["country"],"name":[1],"type":["fctr"],"align":["left"]},{"label":["continent"],"name":[2],"type":["fctr"],"align":["left"]},{"label":["year"],"name":[3],"type":["int"],"align":["right"]},{"label":["lifeExp"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["pop"],"name":[5],"type":["int"],"align":["right"]},{"label":["gdpPercap"],"name":[6],"type":["dbl"],"align":["right"]},{"label":["loggdp"],"name":[7],"type":["dbl"],"align":["right"]}],"data":[{"1":"Afghanistan","2":"Asia","3":"1952","4":"28.801","5":"8425333","6":"779.4453","7":"6.658583"},{"1":"Afghanistan","2":"Asia","3":"1957","4":"30.332","5":"9240934","6":"820.8530","7":"6.710344"},{"1":"Afghanistan","2":"Asia","3":"1962","4":"31.997","5":"10267083","6":"853.1007","7":"6.748878"},{"1":"Afghanistan","2":"Asia","3":"1967","4":"34.020","5":"11537966","6":"836.1971","7":"6.728864"},{"1":"Afghanistan","2":"Asia","3":"1972","4":"36.088","5":"13079460","6":"739.9811","7":"6.606625"},{"1":"Afghanistan","2":"Asia","3":"1977","4":"38.438","5":"14880372","6":"786.1134","7":"6.667101"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] --- # Logarithms in R II - Note, `log()` by default is the **natural logarithm `\(ln()\)`**, i.e. base `e` - Can change base with e.g. `log(x, base = 5)` - Some common built-in logs: `log10`, `log2` ```r log10(100) ``` ``` ## [1] 2 ``` ```r log2(16) ``` ``` ## [1] 4 ``` ```r log(19683, base=3) ``` ``` ## [1] 9 ``` --- # Logarithms in R III - Note when running a regression, you can pre-transform the data into logs (as I did above), or just add `log()` around a variable in the regression .pull-left[ .tiny[ ```r lm(lifeExp ~ loggdp, data = gapminder) %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"-9.100889","3":"1.227674","4":"-7.413117","5":"1.934812e-13"},{"1":"loggdp","2":"8.405085","3":"0.148762","4":"56.500206","5":"0.000000e+00"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .tiny[ ```r lm(lifeExp ~ log(gdpPercap), data = gapminder) %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"-9.100889","3":"1.227674","4":"-7.413117","5":"1.934812e-13"},{"1":"log(gdpPercap)","2":"8.405085","3":"0.148762","4":"56.500206","5":"0.000000e+00"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] --- # Types of Logarithmic Models - Three types of log regression models, depending on which variables we log -- 1. .hi-purple[Linear-log model:] `\(Y_i=\beta_0+\beta_1 \color{#e64173}{\ln X_i}\)` -- 2. .hi-purple[Log-linear model:] `\(\color{#e64173}{\ln Y_i}=\beta_0+\beta_1X_i\)` -- 3. .hi-purple[Log-log model:] `\(\color{#e64173}{\ln Y_i}=\beta_0+\beta_1 \color{#e64173}{\ln X_i}\)` --- class: inverse, center, middle # Linear-Log Model --- # Linear-Log Model - .hi-purple[Linear-log model] has an independent variable `\((X)\)` that is logged -- `$$\begin{align*} Y&=\beta_0+\beta_1 \color{#e64173}{\ln X_i}\\ \beta_1&=\cfrac{\Delta Y}{\big(\frac{\Delta X}{X}\big)}\\ \end{align*}$$` -- - .hi-purple[**Marginal effect of** `\\(\mathbf{X \rightarrow Y}\\)`: a **1%** change in `\\(X \rightarrow\\)` a `\\(\frac{\beta_1}{100}\\)` **unit** change in `\\(Y\\)`] --- # Linear-Log Model in R .pull-left[ .tiny[ ```r lin_log_reg <- lm(lifeExp ~ loggdp, data = gapminder) library(broom) lin_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"-9.100889","3":"1.227674","4":"-7.413117","5":"1.934812e-13"},{"1":"loggdp","2":"8.405085","3":"0.148762","4":"56.500206","5":"0.000000e+00"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{Life Expectancy}}_i=-9.10+9.41 \, \text{ln GDP}_i$$` ] ] --- # Linear-Log Model in R .pull-left[ .tiny[ ```r lin_log_reg <- lm(lifeExp ~ loggdp, data = gapminder) library(broom) lin_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"-9.100889","3":"1.227674","4":"-7.413117","5":"1.934812e-13"},{"1":"loggdp","2":"8.405085","3":"0.148762","4":"56.500206","5":"0.000000e+00"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{Life Expectancy}}_i=-9.10+9.41 \, \text{ln GDP}_i$$` - A **1% change in GDP** `\(\rightarrow\)` a `\(\frac{9.41}{100}=\)` **0.0941 year increase** in Life Expectancy ] ] --- # Linear-Log Model in R .pull-left[ .tiny[ ```r lin_log_reg <- lm(lifeExp ~ loggdp, data = gapminder) library(broom) lin_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"-9.100889","3":"1.227674","4":"-7.413117","5":"1.934812e-13"},{"1":"loggdp","2":"8.405085","3":"0.148762","4":"56.500206","5":"0.000000e+00"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{Life Expectancy}}_i=-9.10+9.41 \, \text{ln GDP}_i$$` - A **1% change in GDP** `\(\rightarrow\)` a `\(\frac{9.41}{100}=\)` **0.0941 year increase** in Life Expectancy - A **25% fall in GDP** `\(\rightarrow\)` a `\((-25 \times 0.0941)=\)` **2.353 year decrease** in Life Expectancy ] ] --- # Linear-Log Model in R .pull-left[ .tiny[ ```r lin_log_reg <- lm(lifeExp ~ loggdp, data = gapminder) library(broom) lin_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"-9.100889","3":"1.227674","4":"-7.413117","5":"1.934812e-13"},{"1":"loggdp","2":"8.405085","3":"0.148762","4":"56.500206","5":"0.000000e+00"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{Life Expectancy}}_i=-9.10+9.41 \, \text{ln GDP}_i$$` - A **1% change in GDP** `\(\rightarrow\)` a `\(\frac{9.41}{100}=\)` **0.0941 year increase** in Life Expectancy - A **25% fall in GDP** `\(\rightarrow\)` a `\((-25 \times 0.0941)=\)` **2.353 year decrease** in Life Expectancy - A **100% rise in GDP** `\(\rightarrow\)` a `\((100 \times 0.0941)=\)` **9.041 year increase** in Life Expectancy ] ] --- # Linear-Log Model Graph I .pull-left[ .code50[ ```r ggplot(data = gapminder)+ aes(x = gdpPercap, y = lifeExp)+ geom_point(color="blue", alpha=0.5)+ * geom_smooth(method="lm", * formula=y~log(x), * color="orange")+ scale_x_continuous(labels=scales::dollar, breaks=seq(0,120000,20000))+ scale_y_continuous(breaks=seq(0,100,10), limits=c(0,100))+ labs(x = "GDP per Capita", y = "Life Expectancy (Years)")+ ggthemes::theme_pander(base_family = "Fira Sans Condensed", base_size=16) ``` ] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-16-1.png" width="504" /> ] --- # Linear-Log Model Graph II .pull-left[ .code50[ ```r ggplot(data = gapminder)+ * aes(x = loggdp, y = lifeExp)+ geom_point(color="blue", alpha=0.5)+ * geom_smooth(method="lm", color="orange")+ scale_y_continuous(breaks=seq(0,100,10), limits=c(0,100))+ labs(x = "Log GDP per Capita", y = "Life Expectancy (Years)")+ ggthemes::theme_pander(base_family = "Fira Sans Condensed", base_size=16) ``` ] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-17-1.png" width="504" /> ] --- class: inverse, center, middle # Log-Linear Model --- # Log-Linear Model - .hi-purple[Log-linear model] has the dependent variable `\((Y)\)` logged -- `$$\begin{align*} \color{#e64173}{\ln Y_i}&=\beta_0+\beta_1 X\\ \beta_1&=\cfrac{\big(\frac{\Delta Y}{Y}\big)}{\Delta X}\\ \end{align*}$$` -- - .hi-purple[**Marginal effect of** `\\(\mathbf{X \rightarrow Y}\\)`: a **1 unit** change in `\\(X \rightarrow\\)` a `\\(\beta_1 \times 100\\)` **%** change in `\\(Y\\)`] --- # Log-Linear Model in R (Preliminaries) .smallest[ - We will again have very large/small coefficients if we deal with GDP directly, again let's transform `gdpPercap` into $1,000s, call it `gdp_t` - Then log LifeExp ] -- .quitesmall[ ```r gapminder <- gapminder %>% mutate(gdp_t = gdpPercap/1000, # first make GDP/capita in $1000s loglife = log(lifeExp)) # take the log of LifeExp gapminder %>% head() # look at it ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["country"],"name":[1],"type":["fctr"],"align":["left"]},{"label":["continent"],"name":[2],"type":["fctr"],"align":["left"]},{"label":["year"],"name":[3],"type":["int"],"align":["right"]},{"label":["lifeExp"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["pop"],"name":[5],"type":["int"],"align":["right"]},{"label":["gdpPercap"],"name":[6],"type":["dbl"],"align":["right"]},{"label":["loggdp"],"name":[7],"type":["dbl"],"align":["right"]},{"label":["gdp_t"],"name":[8],"type":["dbl"],"align":["right"]},{"label":["loglife"],"name":[9],"type":["dbl"],"align":["right"]}],"data":[{"1":"Afghanistan","2":"Asia","3":"1952","4":"28.801","5":"8425333","6":"779.4453","7":"6.658583","8":"0.7794453","9":"3.360410"},{"1":"Afghanistan","2":"Asia","3":"1957","4":"30.332","5":"9240934","6":"820.8530","7":"6.710344","8":"0.8208530","9":"3.412203"},{"1":"Afghanistan","2":"Asia","3":"1962","4":"31.997","5":"10267083","6":"853.1007","7":"6.748878","8":"0.8531007","9":"3.465642"},{"1":"Afghanistan","2":"Asia","3":"1967","4":"34.020","5":"11537966","6":"836.1971","7":"6.728864","8":"0.8361971","9":"3.526949"},{"1":"Afghanistan","2":"Asia","3":"1972","4":"36.088","5":"13079460","6":"739.9811","7":"6.606625","8":"0.7399811","9":"3.585960"},{"1":"Afghanistan","2":"Asia","3":"1977","4":"38.438","5":"14880372","6":"786.1134","7":"6.667101","8":"0.7861134","9":"3.649047"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] --- # Log-Linear Model in R .pull-left[ .tiny[ ```r log_lin_reg<-lm(loglife~gdp_t, data = gapminder) tidy(log_lin_reg) ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"3.966639","3":"0.0058345501","4":"679.85339","5":"0.000000e+00"},{"1":"gdp_t","2":"0.012917","3":"0.0004777072","4":"27.03958","5":"2.920378e-134"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\ln\text{Life Expectancy}}_i=3.967+0.013 \, \text{GDP}_i$$` ] ] --- # Log-Linear Model in R .pull-left[ .tiny[ ```r log_lin_reg <- lm(loglife ~ gdp_t, data = gapminder) log_lin_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"3.966639","3":"0.0058345501","4":"679.85339","5":"0.000000e+00"},{"1":"gdp_t","2":"0.012917","3":"0.0004777072","4":"27.03958","5":"2.920378e-134"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\ln\text{Life Expectancy}}_i=3.967+0.013 \, \text{GDP}_i$$` - A **$1 (thousand) change in GDP** `\(\rightarrow\)` a `\(0.013 \times 100\%=\)` **1.3% increase** in Life Expectancy ] ] --- # Log-Linear Model in R .pull-left[ .tiny[ ```r log_lin_reg <- lm(loglife ~ gdp_t, data = gapminder) log_lin_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"3.966639","3":"0.0058345501","4":"679.85339","5":"0.000000e+00"},{"1":"gdp_t","2":"0.012917","3":"0.0004777072","4":"27.03958","5":"2.920378e-134"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{ln(\text{Life Expectancy})}_i=3.967+0.013 \, \text{GDP}_i$$` - A **$1 (thousand) change in GDP** `\(\rightarrow\)` a `\(0.013 \times 100\%=\)` **1.3% increase** in Life Expectancy - A **$25 (thousand) fall in GDP** `\(\rightarrow\)` a `\((-25 \times 1.3\%)=\)` **32.5% decrease** in Life Expectancy ] ] --- # Log-Linear Model in R .pull-left[ .tiny[ ```r log_lin_reg <- lm(loglife ~ gdp_t, data = gapminder) log_lin_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"3.966639","3":"0.0058345501","4":"679.85339","5":"0.000000e+00"},{"1":"gdp_t","2":"0.012917","3":"0.0004777072","4":"27.03958","5":"2.920378e-134"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{ln(\text{Life Expectancy})}_i=3.967+0.013 \, \text{GDP}_i$$` - A **$1 (thousand) change in GDP** `\(\rightarrow\)` a `\(0.013 \times 100\%=\)` **1.3% increase** in Life Expectancy - A **$25 (thousand) fall in GDP** `\(\rightarrow\)` a `\((-25 \times 1.3\%)=\)` **32.5% decrease** in Life Expectancy - A **$100 (thousand) rise in GDP** `\(\rightarrow\)` a `\((100 \times 1.3\%)=\)` **130% increase** in Life Expectancy ] ] --- # Linear-Log Model Graph I .pull-left[ .code50[ ```r ggplot(data = gapminder)+ * aes(x = gdp_t, * y = loglife)+ geom_point(color="blue", alpha=0.5)+ * geom_smooth(method="lm", color="orange")+ scale_x_continuous(labels=scales::dollar, breaks=seq(0,120,20))+ labs(x = "GDP per Capita ($ Thousands)", y = "Log Life Expectancy")+ ggthemes::theme_pander(base_family = "Fira Sans Condensed", base_size=16) ``` ] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-23-1.png" width="504" /> ] --- class: inverse, center, middle # Log-Log Model --- # Log-Log Model - .hi-purple[Log-log model] has both variables `\((X \text{ and } Y)\)` logged -- `$$\begin{align*} \color{#e64173}{\ln Y_i}&=\beta_0+\beta_1 \color{#e64173}{\ln X_i}\\ \beta_1&=\cfrac{\big(\frac{\Delta Y}{Y}\big)}{\big(\frac{\Delta X}{X}\big)}\\ \end{align*}$$` -- - .hi-purple[**Marginal effect of** `\\(\mathbf{X \rightarrow Y}\\)`: a **1%** change in `\\(X \rightarrow\\)` a `\\(\beta_1\\)` **%** change in `\\(Y\\)`] - `\(\beta_1\)` is the .hi-turquoise[elasticity] of `\(Y\)` with respect to `\(X\)`! --- # Log-Log Model in R .pull-left[ .tiny[ ```r log_log_reg <- lm(loglife ~ loggdp, data = gapminder) log_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"2.864177","3":"0.02328274","4":"123.01718","5":"0"},{"1":"loggdp","2":"0.146549","3":"0.00282126","4":"51.94452","5":"0"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{ln Life Expectancy}}_i=2.864+0.147 \, \text{ln GDP}_i$$` ] ] --- # Log-Log Model in R .pull-left[ .tiny[ ```r log_log_reg <- lm(loglife ~ loggdp, data = gapminder) log_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"2.864177","3":"0.02328274","4":"123.01718","5":"0"},{"1":"loggdp","2":"0.146549","3":"0.00282126","4":"51.94452","5":"0"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{ln Life Expectancy}}_i=2.864+0.147 \, \text{ln GDP}_i$$` - A **1% change in GDP** `\(\rightarrow\)` a **0.147% increase** in Life Expectancy ] ] --- # Log-Log Model in R .pull-left[ .tiny[ ```r log_log_reg <- lm(loglife ~ loggdp, data = gapminder) log_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"2.864177","3":"0.02328274","4":"123.01718","5":"0"},{"1":"loggdp","2":"0.146549","3":"0.00282126","4":"51.94452","5":"0"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{ln Life Expectancy}}_i=2.864+0.147 \, \text{ln GDP}_i$$` - A **1% change in GDP** `\(\rightarrow\)` a **0.147% increase** in Life Expectancy - A **25% fall in GDP** `\(\rightarrow\)` a `\((-25 \times 0.147\%)=\)` **3.675% decrease** in Life Expectancy ] ] --- # Log-Log Model in R .pull-left[ .tiny[ ```r log_log_reg <- lm(loglife ~ loggdp, data = gapminder) log_log_reg %>% tidy() ``` <div data-pagedtable="false"> <script data-pagedtable-source type="application/json"> {"columns":[{"label":["term"],"name":[1],"type":["chr"],"align":["left"]},{"label":["estimate"],"name":[2],"type":["dbl"],"align":["right"]},{"label":["std.error"],"name":[3],"type":["dbl"],"align":["right"]},{"label":["statistic"],"name":[4],"type":["dbl"],"align":["right"]},{"label":["p.value"],"name":[5],"type":["dbl"],"align":["right"]}],"data":[{"1":"(Intercept)","2":"2.864177","3":"0.02328274","4":"123.01718","5":"0"},{"1":"loggdp","2":"0.146549","3":"0.00282126","4":"51.94452","5":"0"}],"options":{"columns":{"min":{},"max":[10]},"rows":{"min":[10],"max":[10]},"pages":{}}} </script> </div> ] ] .pull-right[ .smallest[ `$$\widehat{\text{ln Life Expectancy}}_i=2.864+0.147 \, \text{ln GDP}_i$$` - A **1% change in GDP** `\(\rightarrow\)` a **0.147% increase** in Life Expectancy - A **25% fall in GDP** `\(\rightarrow\)` a `\((-25 \times 0.147\%)=\)` **3.675% decrease** in Life Expectancy - A **100% rise in GDP** `\(\rightarrow\)` a `\((100 \times 0.147\%)=\)` **14.7% increase** in Life Expectancy ] ] --- # Log-Log Model Graph I .pull-left[ .code50[ ```r ggplot(data = gapminder)+ * aes(x = loggdp, * y = loglife)+ geom_point(color="blue", alpha=0.5)+ * geom_smooth(method="lm", color="orange")+ labs(x = "Log GDP per Capita", y = "Log Life Expectancy")+ ggthemes::theme_pander(base_family = "Fira Sans Condensed", base_size=16) ``` ] ] .pull-right[ <img src="3.9-slides_files/figure-html/unnamed-chunk-28-1.png" width="504" /> ] --- # Comparing Models I | Model | Equation | Interpretation | |-------|----------|----------------| | Linear-.hi[Log] | `\(Y=\beta_0+\beta_1 \color{#e64173}{\ln X}\)` | 1.hi[%] change in `\(X \rightarrow \frac{\hat{\beta_1}}{100}\)` **unit** change in `\(Y\)` | | .hi[Log]-Linear | `\(\color{#e64173}{\ln Y}=\beta_0+\beta_1X\)` | 1 **unit** change in `\(X \rightarrow \hat{\beta_1}\times 100\)`.hi[%] change in `\(Y\)` | | .hi[Log]-.hi[Log] | `\(\color{#e64173}{\ln Y}=\beta_0+\beta_1\color{#e64173}{\ln X}\)` | 1.hi[%] change in `\(X \rightarrow \hat{\beta_1}\)`.hi[%] change in `\(Y\)` | - Hint: the variable that gets .hi[logged] changes in .hi[percent] terms, the variable not logged changes in **unit** terms --- # Comparing Models II .pull-left[ .code50[ ```r library(huxtable) huxreg("Life Exp." = lin_log_reg, "Log Life Exp." = log_lin_reg, "Log Life Exp." = log_log_reg, coefs = c("Constant" = "(Intercept)", "GDP ($1000s)" = "gdp_t", "Log GDP" = "loggdp"), statistics = c("N" = "nobs", "R-Squared" = "r.squared", "SER" = "sigma"), number_format = 2) ``` ] - Models are very different units, how to choose? - Compare `\\(R^2\\)`’s - Compare graphs - Compare intution ] .pull-left[ .tiny[ <table class="huxtable" style="border-collapse: collapse; border: 0px; margin-bottom: 2em; margin-top: 2em; ; margin-left: auto; margin-right: auto; " id="tab:unnamed-chunk-29"> <col><col><col><col><tr> <th style="vertical-align: top; text-align: center; white-space: normal; border-style: solid solid solid solid; border-width: 0.8pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"></th><th style="vertical-align: top; text-align: center; white-space: normal; border-style: solid solid solid solid; border-width: 0.8pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">Life Exp.</th><th style="vertical-align: top; text-align: center; white-space: normal; border-style: solid solid solid solid; border-width: 0.8pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">Log Life Exp.</th><th style="vertical-align: top; text-align: center; white-space: normal; border-style: solid solid solid solid; border-width: 0.8pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">Log Life Exp.</th></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">Constant</th><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">-9.10 ***</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">3.97 ***</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">2.86 ***</td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"></th><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">(1.23) </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">(0.01) </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">(0.02) </td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">GDP ($1000s)</th><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"> </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.01 ***</td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"> </td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"></th><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"> </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">(0.00) </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"> </td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">Log GDP</th><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">8.41 ***</td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"> </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.15 ***</td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"></th><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">(0.15) </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"> </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">(0.00) </td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">N</th><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">1704 </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">1704 </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">1704 </td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">R-Squared</th><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.65 </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.30 </td><td style="vertical-align: top; text-align: right; white-space: normal; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.61 </td></tr> <tr> <th style="vertical-align: top; text-align: left; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.8pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">SER</th><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.8pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">7.62 </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.8pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.19 </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.8pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.14 </td></tr> <tr> <th colspan="4" style="vertical-align: top; text-align: left; white-space: normal; border-style: solid solid solid solid; border-width: 0.8pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;"> *** p < 0.001; ** p < 0.01; * p < 0.05.</th></tr> </table> ] ] --- # Comparing Models III .smallest[ | Linear-.hi[Log] | .hi[Log]-Linear | .hi[Log]-.hi[Log] | |:----------:|:----------:|:-------:| |  |  |  | | `\(\hat{Y_i}=\hat{\beta_0}+\hat{\beta_1}\color{#e64173}{\ln X_i}\)` | `\(\color{#e64173}{\ln Y_i}=\hat{\beta_0}+\hat{\beta_1}X_i\)` | `\(\color{#e64173}{\ln Y_i}=\hat{\beta_0}+\hat{\beta_1}\color{#e64173}{\ln X_i}\)` | | `\(R^2=0.65\)` | `\(R^2=0.30\)` | `\(R^2=0.61\)` | ] --- # When to Log? .smaller[ - In practice, the following types of variables are logged: - Variables that must always be positive (prices, sales, market values) - Very large numbers (population, GDP) - Variables we want to talk about as percentage changes or growth rates (money supply, population, GDP) - Variables that have diminishing returns (output, utility) - Variables that have nonlinear scatterplots ] -- .smaller[ - Avoid logs for: - Variables that are less than one, decimals, 0, or negative - Categorical variables (season, gender, political party) - Time variables (year, week, day) ] --- class: inverse, center, middle # Comparing Across Units --- # Comparing Coefficients of Different Units I .smallest[ `$$\hat{Y_i}=\beta_0+\beta_1 X_1+\beta_2 X_2 $$` - We often want to compare coefficients to see which variable `\(X_1\)` or `\(X_2\)` has a bigger effect on `\(Y\)` - What if `\(X_1\)` and `\(X_2\)` are different units? .content-box-green[ .green[**Example**]: `$$\begin{align*} \widehat{\text{Salary}_i}&=\beta_0+\beta_1\, \text{Batting average}_i+\beta_2\, \text{Home runs}_i\\ \widehat{\text{Salary}_i}&=-\text{2,869,439.40}+\text{12,417,629.72} \, \text{Batting average}_i+\text{129,627.36}\, \text{Home runs}_i\\ \end{align*}$$` ] ] --- # Comparing Coefficients of Different Units II - An easy way is to .hi[standardize]<sup>.magenta[†]</sup> the variables (i.e. take the `\(Z\)`-score) `$$X^{std}=\frac{X-\overline{X}}{sd(X)}$$` .footnote[<sup>.magenta[†]</sup> Also called “centering” or “scaling.”] --- # Comparing Coefficients of Different Units: Example .smallest[ | Variable | Mean | Std. Dev. | |----------|------|-----------| | Salary | $2,024,616 | $2,764,512 | | Batting Average | 0.267 | 0.031 | | Home Runs | 12.11 | 10.31 | ] .quitesmall[ `$$\begin{align*}\scriptsize \widehat{\text{Salary}_i}&=-\text{2,869,439.40}+\text{12,417,629.72} \, \text{Batting average}_i+\text{129,627.36} \, \text{Home runs}_i\\ \widehat{\text{Salary}_i}^{std}&=\text{0.00}+\text{0.14} \, \text{Batting average}_i^{std}+\text{0.48} \, \text{Home runs}_i^{std}\\ \end{align*}$$` ] -- .quitesmall[ - .hi-purple[Marginal effects] on `\(Y\)` (in *standard deviations* of `\(Y\)`) from 1 *standard deviation* change in `\(X\)`: - `\(\hat{\beta_1}\)`: a 1 standard deviation increase in Batting Average increases Salary by 0.14 standard deviations $$0.14 \times \$2,764,512=\$387,032$$ - `\(\hat{\beta_2}\)`: a 1 standard deviation increase in Home Runs increases Salary by 0.48 standard deviations $$0.48 \times \$2,764,512=\$1,326,966$$ ] --- # Standardizing in `R` - Use the `scale()` command inside `mutate()` function to standardize a variable ```r gapminder<-gapminder %>% mutate(std_life = scale(lifeExp), std_gdp = scale(gdpPercap)) std_reg<-lm(std_life~std_gdp, data = gapminder) tidy(std_reg) ``` <table class="huxtable" style="border-collapse: collapse; border: 0px; margin-bottom: 2em; margin-top: 2em; ; margin-left: auto; margin-right: auto; " id="tab:unnamed-chunk-30"> <col><col><col><col><col><tr> <th style="vertical-align: top; text-align: left; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">term</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">estimate</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">std.error</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">statistic</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">p.value</th></tr> <tr> <td style="vertical-align: top; text-align: left; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0.4pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">(Intercept)</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">1.1e-16</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">0.0197</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">5.57e-15</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">1 </td></tr> <tr> <td style="vertical-align: top; text-align: left; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">std_gdp</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.584 </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.0197</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">29.7 </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">3.57e-156</td></tr> </table> --- class: inverse, center, middle # Joint Hypothesis Testing --- # Joint Hypothesis Testing I .content-box-green[ .green[**Example**]: Return again to: `$$\widehat{Wage_i}=\hat{\beta_0}+\hat{\beta_1}Male_i+\hat{\beta_2}Northeast_i+\hat{\beta_3}Midwest_i+\hat{\beta_4}South_i$$` ] -- - Maybe region doesn't affect wages *at all*? -- - `\(H_0: \beta_2=0, \, \beta_3=0, \, \beta_4=0\)` -- - This is a .hi[joint hypothesis] to test --- # Joint Hypothesis Testing II - A .hi[joint hypothesis] tests against the null hypothesis of a value for *multiple* parameters: `$$\mathbf{H_0: \beta_1= \beta_2=0}$$` the hypotheses that multiple regressors are equal to zero (have no causal effect on the outcome) -- - Our **alternative hypothesis** is that: `$$H_1: \text{ either } \beta_1\neq0\text{ or } \beta_2\neq0\text{ or both}$$` or simply, that `\(H_0\)` is not true --- # Types of Joint Hypothesis Tests .smallest[ - Three main cases of joint hypothesis tests: ] -- .smallest[ 1) `\(H_0\)`: `\(\beta_1=\beta_2=0\)` - Testing against the claim that multiple variables don't matter - Useful under high multicollinearity between variables - `\(H_a\)`: at least one parameter `\(\neq\)` 0 ] -- .smallest[ 2) `\(H_0\)`: `\(\beta_1=\beta_2\)` - Testing whether two variables matter the same - Variables must be the same units - `\(H_a: \beta_1 (\neq, <, \text{ or }>) \beta_2\)` ] -- .smallest[ 3) `\(H_0:\)` ALL `\(\beta\)`'s `\(=0\)` - The "**Overall F-test"** - Testing against claim that regression model explains *NO* variation in `\(Y\)` ] --- # Joint Hypothesis Tests: F-statistic - The .hi-turquoise[F-statistic] is the test-statistic used to test joint hypotheses about regression coefficients with an .hi-turquoise[F-test] -- - This involves comparing two models: 1. .hi[Unrestricted model]: regression with all coefficients 2. .hi-purple[Restricted model]: regression under null hypothesis (coefficients equal hypothesized values) -- - `\(F\)` is an .hi-turquoise[analysis of variance (ANOVA)] - essentially tests whether `\(R^2\)` increases statistically significantly as we go from the restricted model$\rightarrow$unrestricted model -- - `\(F\)` has its own distribution, with *two* sets of degrees of freedom --- # Joint Hypothesis F-test: Example I .content-box-green[ .green[**Example**]: Return again to: `$$\widehat{Wage_i}=\hat{\beta_0}+\hat{\beta_1}Male_i+\hat{\beta_2}Northeast_i+\hat{\beta_3}Midwest_i+\hat{\beta_4}South_i$$` ] -- - `\(H_0: \beta_2=\beta_3=\beta_4=0\)` -- - `\(H_a\)`: `\(H_0\)` is not true (at least one `\(\beta_i \neq 0\)`) --- # Joint Hypothesis F-test: Example II .smallest[ .content-box-green[ .green[**Example**]: Return again to: `$$\widehat{Wage_i}=\hat{\beta_0}+\hat{\beta_1}Male_i+\hat{\beta_2}Northeast_i+\hat{\beta_3}Midwest_i+\hat{\beta_4}South_i$$` ] - .hi[Unrestricted model]: `$$\widehat{Wage_i}=\hat{\beta_0}+\hat{\beta_1}Male_i+\hat{\beta_2}Northeast_i+\hat{\beta_3}Midwest_i+\hat{\beta_4}South_i$$` ] -- .smallest[ - .hi-purple[Restricted model]: `$$\widehat{Wage_i}=\hat{\beta_0}+\hat{\beta_1}Male_i$$` ] -- .smallest[ - `\(F\)`: does going from .hi-purple[restricted] to .hi[unrestricted] model statistically significantly improve `\(R^2\)`? ] --- # Calculating the F-statistic .pull-left[ `$$F_{q,(n-k-1)}=\cfrac{\left(\displaystyle\frac{(R^2_u-R^2_r)}{q}\right)}{\left(\displaystyle\frac{(1-R^2_u)}{(n-k-1)}\right)}$$` ] .pull-right[ ] --- # Calculating the F-statistic .pull-left[ `$$F_{q,(n-k-1)}=\cfrac{\left(\displaystyle\frac{(\color{#e64173}{R^2_u}-R^2_r)}{q}\right)}{\left(\displaystyle\frac{(1-\color{#e64173}{R^2_u})}{(n-k-1)}\right)}$$` ] .pull-right[ - `\(\color{#e64173}{R^2_u}\)`: the `\(R^2\)` from the .hi[unrestricted model] (all variables) ] --- # Calculating the F-statistic .pull-left[ `$$F_{q,(n-k-1)}=\cfrac{\left(\displaystyle\frac{(\color{#e64173}{R^2_u}-\color{#6A5ACD}{R^2_r})}{q}\right)}{\left(\displaystyle\frac{(1-\color{#e64173}{R^2_u})}{(n-k-1)}\right)}$$` ] .pull-right[ - `\(\color{#e64173}{R^2_u}\)`: the `\(R^2\)` from the .hi[unrestricted model] (all variables) - `\(\color{#6A5ACD}{R^2_r}\)`: the `\(R^2\)` from the .hi-purple[restricted model] (null hypothesis) ] --- # Calculating the F-statistic .pull-left[ `$$F_{q,(n-k-1)}=\cfrac{\left(\displaystyle\frac{(\color{#e64173}{R^2_u}-\color{#6A5ACD}{R^2_r})}{q}\right)}{\left(\displaystyle\frac{(1-\color{#e64173}{R^2_u})}{(n-k-1)}\right)}$$` ] .pull-right[ - `\(\color{#e64173}{R^2_u}\)`: the `\(R^2\)` from the .hi[unrestricted model] (all variables) - `\(\color{#6A5ACD}{R^2_r}\)`: the `\(R^2\)` from the .hi-purple[restricted model] (null hypothesis) - `\(q\)`: number of restrictions (number of `\(\beta's=0\)` under null hypothesis) ] --- # Calculating the F-statistic .pull-left[ `$$F_{q,(n-k-1)}=\cfrac{\left(\displaystyle\frac{(\color{#e64173}{R^2_u}-\color{#6A5ACD}{R^2_r})}{q}\right)}{\left(\displaystyle\frac{(1-\color{#e64173}{R^2_u})}{(n-k-1)}\right)}$$` ] .pull-right[ - `\(\color{#e64173}{R^2_u}\)`: the `\(R^2\)` from the .hi[unrestricted model] (all variables) - `\(\color{#6A5ACD}{R^2_r}\)`: the `\(R^2\)` from the .hi-purple[restricted model] (null hypothesis) - `\(q\)`: number of restrictions (number of `\(\beta's=0\)` under null hypothesis) - `\(k\)`: number of `\(X\)` variables in .hi[unrestricted model] (all variables) ] --- # Calculating the F-statistic .pull-left[ `$$F_{q,(n-k-1)}=\cfrac{\left(\displaystyle\frac{(\color{#e64173}{R^2_u}-\color{#6A5ACD}{R^2_r})}{q}\right)}{\left(\displaystyle\frac{(1-\color{#e64173}{R^2_u})}{(n-k-1)}\right)}$$` ] .pull-right[ - `\(\color{#e64173}{R^2_u}\)`: the `\(R^2\)` from the .hi[unrestricted model] (all variables) - `\(\color{#6A5ACD}{R^2_r}\)`: the `\(R^2\)` from the .hi-purple[restricted model] (null hypothesis) - `\(q\)`: number of restrictions (number of `\(\beta's=0\)` under null hypothesis) - `\(k\)`: number of `\(X\)` variables in .hi[unrestricted model] (all variables) .smallest[ - `\(F\)` has two sets of degrees of freedom: - `\(q\)` for the numerator, `\((n-k-1)\)` for the denominator ] ] --- # Calculating the F-statistic II .pull-left[ `$$F_{q,(n-k-1)}=\cfrac{\left(\displaystyle\frac{(R^2_u-R^2_r)}{q}\right)}{\left(\displaystyle\frac{(1-R^2_u)}{(n-k-1)}\right)}$$` ] .pull-right[ - .hi-purple[Key takeaway]: The bigger the difference between `\((R^2_u-R^2_r)\)`, the greater the improvement in fit by adding variables, the larger the `\(F\)`! - This formula is (believe it or not) actually a simplified version (assuming homoskedasticity) - I give you this formula to **build your intuition of what F is measuring** ] --- # F-test Example I - We'll use the `wooldridge` package's `wage1` data again ```r # load in data from wooldridge package library(wooldridge) wages<-wooldridge::wage1 # run regressions unrestricted_reg<-lm(wage~female+northcen+west+south, data=wages) restricted_reg<-lm(wage~female, data=wages) ``` --- # F-test Example II - .hi[Unrestricted model]: `$$\widehat{Wage_i}=\hat{\beta_0}+\hat{\beta_1}Female_i+\hat{\beta_2}Northeast_i+\hat{\beta_3}Northcen+\hat{\beta_4}South_i$$` - .hi-purple[Restricted model]: `$$\widehat{Wage_i}=\hat{\beta_0}+\hat{\beta_1}Female_i$$` - `\(H_0: \beta_2 = \beta_3 = \beta_4 =0\)` - `\(q = 3\)` restrictions (F numerator df) - `\(n-k-1 = 526-4-1=521\)` (F denominator df) --- # F-test Example III - We can use the `car` package's `linearHypothesis()` command to run an `\(F\)`-test: - first argument: name of the (unrestricted) regression - second argument: vector of variable names (in quotes) you are testing ```r # load car package for additional regression tools library("car") # F-test linearHypothesis(unrestricted_reg, c("northcen", "west", "south")) ``` <table class="huxtable" style="border-collapse: collapse; border: 0px; margin-bottom: 2em; margin-top: 2em; ; margin-left: auto; margin-right: auto; " id="tab:unnamed-chunk-32"> <col><col><col><col><col><col><tr> <th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Res.Df</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">RSS</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Df</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Sum of Sq</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">F</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Pr(>F)</th></tr> <tr> <td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0.4pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">524</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">6.33e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"></td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"></td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"> </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"> </td></tr> <tr> <td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">521</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">6.17e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">3</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">157</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">4.43</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.00438</td></tr> </table> --- # Second F-test Example: Are Two Coefficients Equal? .smallest[ - The second type of test is whether two coefficients equal one another .content-box-green[ .green[**Example**]: `$$\widehat{wage_i}=\beta_0+\beta_1 \text{Adolescent height}_i + \beta_2 \text{Adult height}_i + \beta_3 \text{Male}_i$$` ] ] -- .smallest[ - Does height as an adolescent have the same effect on wages as height as an adult? `$$H_0: \beta_1=\beta_2$$` ] -- .smallest[ - What is the .hi-purple[restricted] regression? `$$\widehat{wage_i}=\beta_0+\beta_1(\text{Adolescent height}_i + \text{Adult height}_i )+ \beta_3 \text{Male}_i$$` - `\(q=1\)` restriction ] --- # Second F-test Example: Data ```r # load in data heightwages<-read_csv("../data/heightwages.csv") # make a "heights" variable as the sum of adolescent (height81) and adult (height85) height heightwages <- heightwages %>% mutate(heights=height81+height85) height_reg<-lm(wage96~height81+height85+male, data=heightwages) height_restricted_reg<-lm(wage96~heights+male, data=heightwages) ``` --- # Second F-test Example: Data - For second argument, set two variables equal, in quotes ```r linearHypothesis(height_reg, "height81=height85") # F-test ``` <table class="huxtable" style="border-collapse: collapse; border: 0px; margin-bottom: 2em; margin-top: 2em; ; margin-left: auto; margin-right: auto; " id="tab:unnamed-chunk-34"> <col><col><col><col><col><col><tr> <th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Res.Df</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">RSS</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Df</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Sum of Sq</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">F</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">Pr(>F)</th></tr> <tr> <td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0.4pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">6.59e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">5.13e+06</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"></td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"></td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"> </td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;"> </td></tr> <tr> <td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">6.59e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">5.13e+06</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">1</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">959</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">1.23</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: normal;">0.267</td></tr> </table> - Insufficient evidence to reject `\(H_0\)`! - The effect of adolescent and adult height on wages is the same --- # All F-test I .pull-left[ .code50[ ```r summary(unrestricted_reg) ``` ``` ## ## Call: ## lm(formula = wage ~ female + northcen + west + south, data = wages) ## ## Residuals: ## Min 1Q Median 3Q Max ## -6.3269 -2.0105 -0.7871 1.1898 17.4146 ## ## Coefficients: ## Estimate Std. Error t value Pr(>|t|) ## (Intercept) 7.5654 0.3466 21.827 <2e-16 *** ## female -2.5652 0.3011 -8.520 <2e-16 *** ## northcen -0.5918 0.4362 -1.357 0.1755 ## west 0.4315 0.4838 0.892 0.3729 ## south -1.0262 0.4048 -2.535 0.0115 * ## --- ## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1 ## ## Residual standard error: 3.443 on 521 degrees of freedom ## Multiple R-squared: 0.1376, Adjusted R-squared: 0.131 ## F-statistic: 20.79 on 4 and 521 DF, p-value: 6.501e-16 ``` ] ] .pull-right[ .smallest[ - Last line of regression output from `summary()` is an **All F-test** - `\(H_0:\)` all `\(\beta's=0\)` - the regression explains no variation in `\(Y\)` - Calculates an `F-statistic` that, if high enough, is significant (`p-value` `\(<0.05)\)` enough to reject `\(H_0\)` ] ] --- # All F-test II - Alternatively, if you use `broom` instead of `summary()`: - `glance()` command makes table of regression summary statistics - `tidy()` only shows coefficients .quitesmall[ ```r library(broom) glance(unrestricted_reg) ``` <table class="huxtable" style="border-collapse: collapse; border: 0px; margin-bottom: 2em; margin-top: 2em; ; margin-left: auto; margin-right: auto; " id="tab:unnamed-chunk-36"> <col><col><col><col><col><col><col><col><col><col><col><col><tr> <th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">r.squared</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">adj.r.squared</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">sigma</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">statistic</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">p.value</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">df</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">logLik</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">AIC</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">BIC</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">deviance</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">df.residual</th><th style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; font-weight: bold;">nobs</th></tr> <tr> <td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0.4pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">0.138</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">0.131</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">3.44</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">20.8</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">6.5e-16</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">4</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">-1.39e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">2.8e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">2.83e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">6.17e+03</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">521</td><td style="vertical-align: top; text-align: right; white-space: normal; border-style: solid solid solid solid; border-width: 0.4pt 0.4pt 0.4pt 0pt; padding: 6pt 6pt 6pt 6pt; background-color: rgb(242, 242, 242); font-weight: normal;">526</td></tr> </table> ] - "`statistic`" is the All F-test, "`p.value`" next to it is the p value from the F test